Article

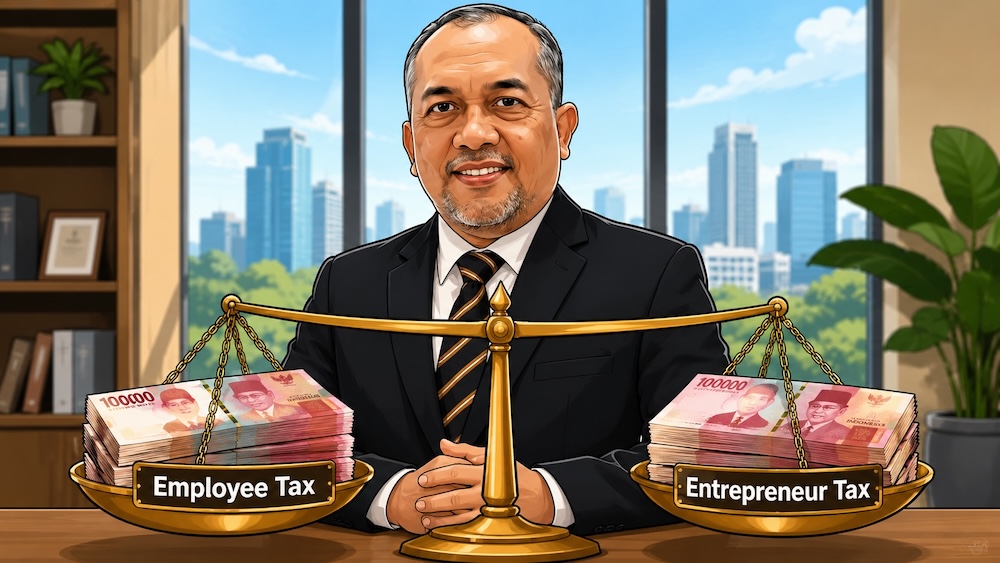

Employee vs. Entrepreneur: Who Bears the Heavier Tax Burden in Indonesia?

Author: Agus Budi Harto, 2026-06-03 22:18:13

When it comes to building wealth in Indonesia, a crucial but often overlooked factor is how the Directorate General of Taxes (Direktorat Jenderal Pajak) treats your income. A common debate among professionals centers on who actually pays more tax: the corporate employee climbing the ladder or the entrepreneur building a business. While the knee-jerk reaction might be that profitable business owners contribute more, Indonesia’s current tax architecture reveals a system where individual employees frequently shoulder a heavier, less flexible tax burden relative to their net income.

To understand why employees often pay more, one must look at how the taxable base is calculated. For a salaried employee, income tax (PPh Pasal 21) is deducted directly from their gross salary by the employer. The government grants very minimal deductions—primarily the standard non-taxable income threshold (PTKP) and a capped occupational expense allowance (Biaya Jabatan) of just IDR 6 million annually. This means almost the entire paycheck is exposed to Indonesia’s progressive tax rates under the Harmonized Tax Law (UU HPP), which quickly scale from 5% up to 35% for high earners. Employees lack the legal mechanisms to write off their daily operational costs, even if those expenses—like internet, transportation, and laptops—are essential to perform their jobs.

In sharp contrast, entrepreneurs and business owners operate under a highly accommodating tax regime designed to stimulate economic growth. Under the government's micro, small, and medium enterprise (MSME) scheme governed by Government Regulation No. 55 of 2022 (PP 55/2022), individual entrepreneurs enjoy a flat final tax rate of just 0.5% on their gross turnover. More importantly, the law grants individual MSMEs a tax-free threshold on their first IDR 500 million of annual revenue. Even when a business expands beyond the MSME threshold and switches to corporate tax filing, the business owner can legally deduct all expenses incurred to "get, collect, and maintain" revenue. Business owners can categorize rent, employee salaries, utility bills, inventory, and even company vehicles as tax-deductible expenses, effectively minimizing their taxable net profit.

The disparity becomes starkly obvious when simulating a side-by-side comparison of an executive and an entrepreneur earning the same revenue baseline of IDR 600 million in a year. The employee, after adjusting for standard PTKP, will see their income subject to progressive brackets, resulting in an annual tax bill that easily reaches tens of millions of rupiah. Meanwhile, the individual entrepreneur utilizing the MSME facility pays absolutely zero tax on the first IDR 500 million, and a mere 0.5% on the remaining IDR 100 million—culminating in a total annual tax liability of just IDR 500,000. This structural design means that at low-to-mid income levels, the tax system heavily favors entrepreneurship over traditional employment.

However, the scales inevitably tip as a business scales up. If an entrepreneur operates as a formal legal entity, such as a Perusahaan Terbatas (PT), they face a corporate income tax rate of 22% on net profits, alongside obligations to collect and remit an 11% Value Added Tax (PPN) once annual revenue crosses IDR 4.8 billion. Furthermore, when the business owner withdraws profits as personal dividends, they may face an additional 10% dividend tax unless those funds are reinvested into specific domestic instruments within Indonesia. Therefore, while micro-entrepreneurs enjoy massive tax advantages, large-scale business owners eventually face a highly complex, multi-layered tax ecosystem that can eclipse individual employment taxes in pure nominal volume.

Ultimately, deciding which path is more tax-efficient depends entirely on your financial scale and long-term goals. For professionals looking to optimize their tax exposure, transitioning from a pure salaried employee to an independent consultant or establishing an MSME structure can unlock significant legal tax-saving mechanisms in Indonesia. Navigating these compliance pathways requires a strategic understanding of domestic tax laws to ensure that your chosen career or business model aligns harmoniously with your wealth-building objectives.

References

- Law of the Republic of Indonesia Number 7 of 2021 concerning the Harmonization of Tax Regulations (Undang-Undang Nomor 7 Tahun 2021 tentang Harmonisasi Peraturan Perpajakan / UU HPP).

- Government Regulation Number 55 of 2022 concerning Adjustments of Regulations in the Field of Income Tax (Peraturan Pemerintah Nomor 55 Tahun 2022 tentang Penyesuaian Pengaturan di Bidang Pajak Penghasilan).

- Directorate General of Taxes (Direktorat Jenderal Pajak) official guidelines on Income Tax Article 21 (PPh Pasal 21) and individual taxpayer obligations.

- Ministry of Finance of the Republic of Indonesia (Kemenkeu) press releases and circulars regarding tax incentives for Micro, Small, and Medium Enterprises (MSMEs).

Add comment

- Other Article

- Rethinking Civil Service Workforce Planning in Indonesia: Beyond Headcount Toward Public Service Capacity31 Jul 2026

- Balancing the Plate: Understanding Daily Nutritional Needs and the Rise of Digital Nutrition Estimation Tools25 Jul 2026

- The Final Four: Strengths, Weaknesses, and Machine Predictions for the 2026 FIFA World Cup18 Jul 2026

- Choosing the Right Framework: A Practical Guide to Best-Practice Problem-Solving Models12 Jul 2026

- Can Science Predict the World Cup? A Look at the Models Behind the 2026 Forecasts04 Jul 2026

- Corruption: A Global Plague, Landmark Cases, and the Path to Prevention27 Jun 2026

- Nations Driving Brilliant Business Ideas and Frameworks in 202620 Jun 2026

- Why the USD Stands Stronger than the IDR — and What Indonesia Can Do13 Jun 2026

- Employee vs. Entrepreneur: Who Bears the Heavier Tax Burden in Indonesia?03 Jun 2026

- The Evolution of Control Operating Centers (COC) in Modern Mining Operations24 May 2026

- Song of: Mariana Istriku13 May 2026

- Organisasi Pensiunan di Indonesia: Dari Komunitas Sosial Menuju Kekuatan Ekonomi Berbasis Pengalaman12 May 2026

- Corporate Risk Management: Why Modern Companies Invest Millions to Prevent Invisible Threats07 May 2026

- The Mining Spirit: A Powerful Mindset for Excellence in the Mining Industry25 Apr 2026

- The Double-Edged Sword: Navigating Competition in the Modern Corporate Landscape22 Apr 2026

- AI Chatbot untuk UMKM: Peluang Besar di Era Digital17 Apr 2026

- AI Chatbots in Business: The Global Revolution09 Apr 2026

- The Heartbeat of Your Business: Why the P&L Statement is Non-Negotiable31 Mar 2026

- Why Your New Business Needs a Financial System on Day One26 Mar 2026

- The Link Between Startup Capital, Business Survival, and the Role of Investor Information21 Mar 2026

- Digital Transformation, Digitalization, and Digitization: Why the Difference Matters More Than You Think14 Mar 2026

- From Business Need to Technology Solution07 Mar 2026

- Bridging the Digital Divide: Starlink and the Future of Internet Access in Indonesia27 Feb 2026

- A Long Weekend Getaway to Yogyakarta16 Feb 2026

- Understanding ERP Systems: A Comprehensive Guide for Modern Businesses16 Feb 2026

- Building a Culture of Awareness: Strategic Approaches to HSE and Information Security Campaigns in Modern Organizations10 Feb 2026

- Building an Effective IT Organization in Coal Mining: A Strategic Framework for Growth02 Feb 2026

- The Art and Science of Color Themes in Modern Web Design17 Jan 2026

- IT Outsourcing vs Internal Resources: A Comprehensive Cost and Risk Analysis05 Jan 2026

- The Hidden Dangers of Mishandled Employee Data: When Internal Tables Fall Into the Wrong Hands05 Jan 2026

- Securing SQL Server: A Complete Guide to Database Access Control05 Jan 2026

- Beyond Human Error: Understanding the Complete Security Chain in Information Security01 Jan 2026